- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Exclusive Interview: Behind BlackRock's "Wall Street on the Blockchain"

By 2025, the biggest trend in crypto will shift from the technology itself to its integration with traditional finance.

On one side, crypto investors no longer believe in empty narratives and technology, nor do they invest in meme coins. Instead, they are turning their attention to US stocks with clear business models and actual revenue.

On the other side, many regions around the world still face challenges in easily investing in US stocks. Investors can only participate through certain brokers, facing difficulties with KYC, usability issues, high fees, and more.

A new race track has emerged.

SEC Chairman Paul Atkins predicts that all US stocks will be put on the blockchain in the next two years. Robinhood is building its own chain for tokenizing US stocks, crypto giants like Binance Wallet and Coinbase are entering the space, HyperLiquid has launched US stock perpetual contracts, with a trading volume exceeding $2 billion in 10 days.

Kevin Tang and Wyatt Raich, two veterans from the world's largest asset management company BlackRock, have also joined this "Wall Street on-chain" competition.

Kevin and Wyatt

Kevin is the Senior Director of BlackRock's Digital Assets team, having personally created IBIT, ETHA, and BUIDL and led their commercialization. Wyatt is the tech lead of the crypto division, having written every line of code that powers IBIT, ETHA, and BUIDL. The IBIT they built became the largest Bitcoin ETF and set a record as the fastest ETF to break through $1 trillion in assets under management.

In May of this year, at the peak of IBIT's success, the two chose to leave and establish HelloTrade, an on-chain trading platform for US stock perpetual contracts and RWAs.

While this may seem like a bold move, Kevin has his own insights. To address the after-hours and weekend gaps in the traditional market and enable 24/7 US stock on-chain trading, one must be well-versed in both traditional finance and crypto technology, which is exactly where he and Wyatt shine. Leveraging the compliance intuition and risk control experience accumulated at BlackRock gives HelloTrade the confidence to enter this race track.

"The true competitors of decentralized exchanges are not each other, but rather the traditional Web2 brokers," Kevin bluntly stated in an interview with BlockBeats. "What we aim to do is not just another crypto product but to replicate the Web2 user experience on the Web3 infrastructure."

Kevin's ambition extends far beyond just US stock perpetual contracts. The HelloTrade he envisions is a blockchain-based trading platform that rivals the experience of traditional brokerages and centralized exchanges, attracting millions of users who have never traded on-chain before.

In this exclusive BlockBeats interview, Kevin shared why IBIT became the most successful ETF in history and why he firmly believes that on-chain US stocks and RWAs are the battleground for the next large-scale blockchain adoption.

Here is the interview content.

Leaving BlackRock

BlockBeats: What was your and Wyatt's career path before joining BlackRock?

Kevin: I worked at BlackRock for over ten years. After graduating from college, I spent a year at State Street before joining BlackRock. I started in the research group and later moved to the innovation products group, where I was involved in launching numerous hedge funds, private equity strategies, and mutual funds.

In 2017, a colleague introduced me to Bitcoin and Ethereum, and I was immediately drawn to them. Many of our clients were already concerned about inflation at that time, and Bitcoin, as a potential store of value, caught my special attention. The emergence of Ethereum brought a whole new possibility as it could build decentralized infrastructure and the next generation of financial applications.

At BlackRock, I saw the longstanding pain points in traditional finance and realized that blockchain technology could address these issues. So before joining the digital assets division, I kept a close eye on the crypto market in my spare time.

Eventually, as the third employee in the business group, I joined the BlackRock Digital Assets department. Over the following four and a half years, I focused on building and commercializing IBIT and ETHA, working with clients, partners, and the internal team to bring these products to market.

Wyatt's career path was a bit different from mine. He initially worked on AI and robotics at Lockheed Martin and was later introduced to digital assets by a friend. He quickly delved into it, started writing smart contracts, testing various protocols, and building applications on his own. He then joined BlackRock as one of the first smart contract engineers in the digital assets team, subsequently leading the technical development behind IBIT, ETHA, and BUIDL, helping to build a smart contract system supporting billions of dollars in funds.

We come from different backgrounds, but eventually ended up in the same team as directors, all believing in one thing, that the next generation of the capital market will be built on-chain.

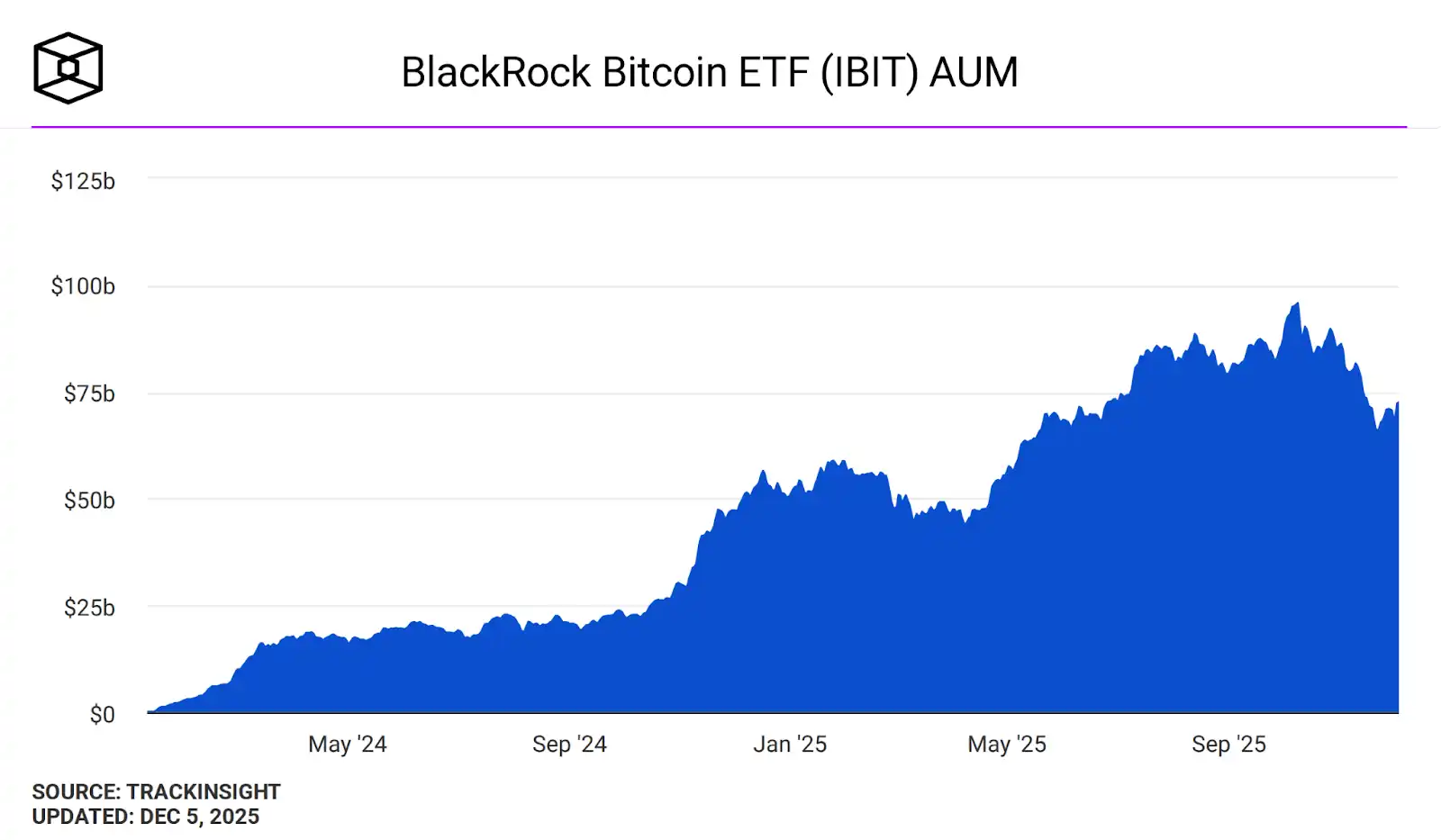

BlockBeats: You built IBIT at BlackRock, which became the world's largest Bitcoin ETF, very successfully. Could you share the story behind this?

Kevin: The success of IBIT and ETHA demonstrates that investors can quickly embrace using an ETF, a convenient and secure way, to invest in spot Bitcoin and Ethereum. For a long time, individuals and institutions faced significant barriers when wanting to directly invest in crypto assets. ETFs utilized a familiar and trustworthy investment tool, solving many issues.

IBIT Growth Rate|Source: Trackinsight

But even though IBIT grew rapidly, it was not easy for BlackRock to venture into crypto products. Before the launch of IBIT, BlackRock had a private Bitcoin trust fund that grew much slower than IBIT.

Many clients required a lot of education: what is the digital asset ecosystem, why Bitcoin and Ethereum deserve a place in the investment portfolio. The entire BlackRock team played a crucial role in educating on these matters.

One more point I would like to make is that from a broader perspective, Bitcoin and Ethereum ETFs are still in the early stages. Most wealth management firms and institutional investors are just beginning to pay attention to crypto assets. In the traditional asset management industry, significant mainstream adoption has yet to begin.

BlockBeats: Since the exploration at BlackRock was so successful, what ultimately led you to leave and believe that products like HelloTrade must be completed on-chain rather than internally at BlackRock?

Kevin: I have always believed that the next major wave of blockchain adoption is moving traditional markets such as stocks, commodities, and fixed income to the blockchain. This is also the reason I ultimately decided to leave BlackRock. Although the number of Americans holding crypto assets has increased, globally, less than 1% of people are actually trading on-chain, and I believe we are still in the very early stages.

HelloTrade has ambitions far beyond perpetual stock contracts. In order to quickly realize all of our ideas, we must rebuild an infrastructure that is not constrained by the frameworks of traditional finance or big tech companies. When settlement, custody, transparency, and access barriers are all redesigned around blockchain, we must rethink from scratch how such an on-chain global market would operate.

The second reason is speed. To achieve our vision, we need to push forward with the fast pace and focus of a small startup, iterate quickly, release new products every few weeks, continuously test with real users in different markets. This agility is hard to achieve in a company of tens of thousands of people.

That being said, we are still very grateful for the experience at BlackRock. It provided us with training, discipline, and a customer-centric mindset, which are the cornerstones of building HelloTrade today.

Global "Wall Street on Chain"

BlockBeats: Let's talk about the product itself. What is the target user of HelloTrade, and what are the main target markets?

Kevin: Let's talk about user personas first. Our long-term goal is to attract two types of people to the chain: one is less experienced crypto users, and the other is traditional financial investors.

When I say "less experienced crypto users," I mean those who basically only trade on centralized exchanges and rarely interact directly with decentralized products on the chain. Currently, the number of CEX traders far exceeds that of DEX.

These people are not professional traders. To attract these users, there must be a familiar interface, similar to traditional internet apps, along with clear risk warnings and reliable security measures, so they can confidently trade on the chain, and this is what we have to provide.

Looking further ahead, we also want to attract a larger group, those who currently only use traditional brokerage platforms.

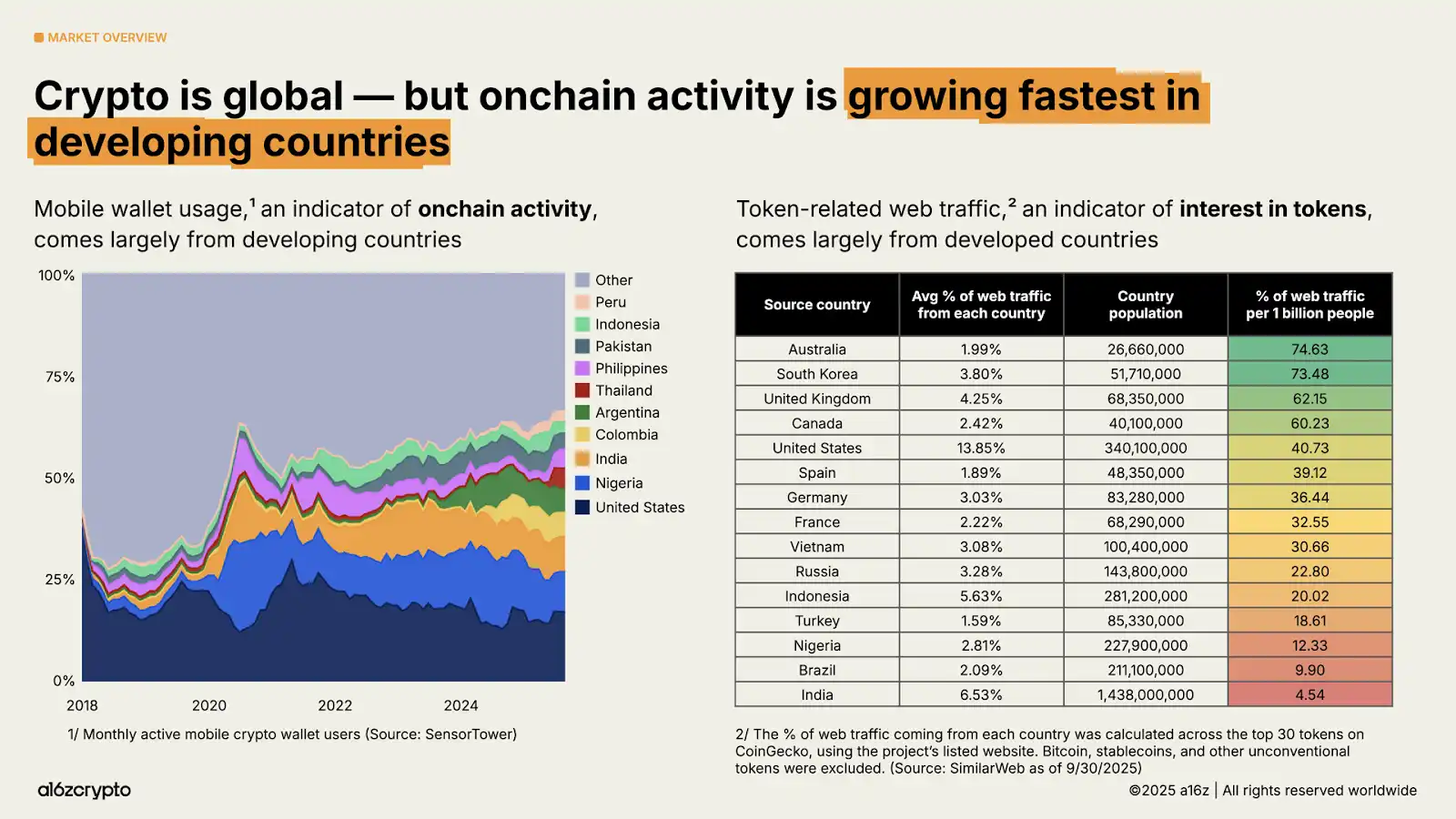

Therefore, in terms of target markets, we focus on regions where access to the global capital market is restricted or costly. In emerging markets such as Southeast Asia, Latin America, and Central Asia, people who want to invest often face many obstacles, such as high fees, fragmented channels, and many financial products that they simply cannot access. An open, global, blockchain-based trading platform can bring the most value to these users.

Rapid Growth of Active On-Chain Users in Emerging Markets|Source: a16zcrypto

BlockBeats: It is very interesting that when I recommend on-chain DEX to friends who are used to Binance and Coinbase, they often ask, "Since I can trade on my phone anytime, why bother opening a website?" How does HelloTrade plan to respond to this question?

Kevin: This question hits the nail on the head, and that's why we are focusing on developing HelloTrade's mobile app. Nowadays, most people are used to trading on their phones rather than websites. The reality is that the interface design, user experience, and reliability of many crypto applications still lag behind those of Web2 apps that everyone is accustomed to.

We aim for HelloTrade to be as user-friendly as any top-notch mobile trading app, while also allowing users to benefit from the advantages of blockchain technology. We will also have a web version, but the mobile app will be our flagship product and the primary way for users to trade on HelloTrade.

In addition to the product experience, we also want to provide real-time customer support. If you encounter an issue, don't know how to use a certain feature on the platform, or feel anxious about on-chain transactions, you should be able to reach a live customer service representative via email, text, or phone. Of course, this is a big plan that may not be fully realized at the initial launch, but it is the direction we are striving towards.

BlockBeats: One of your core products is perpetual contracts, which is a native invention of crypto. As a finance professional from a traditional background, how do you view it?

Kevin: In my opinion, perpetual contracts are the preferred tool for short-term directional leverage exposure. If you want to speculate on the short-term price movement of an underlying asset, I believe perpetual contracts are one of the most effective tools.

For most non-professional traders, the pricing models of options, time decay, and volatility mechanisms may be too complex. Perpetual contracts are much simpler in comparison; they eliminate this complexity, are more linear, easier to understand, and more convenient to manage.

So, in many cases, for traders who simply want to use leverage efficiently and effectively, perpetual contracts are the better tool.

BlockBeats: So, compared to crypto-native perpetual contract products or fintech apps like Robinhood and Revolut, what is HelloTrade's biggest advantage?

Kevin: In fact, I believe our biggest competitor is not other crypto-native Perp Dex, but rather traditional brokers and neobanks like Robinhood and Revolut that people are already very familiar with and trust.

Currently, some Perp Dex have significant trading volume data, but many analyses show that the actual active traders on these platforms are not that many, probably only tens of thousands of active users.

Our core advantage is built on the underlying architecture of Web3, providing a product experience truly comparable to Web2 applications. This means that users here can enjoy a design, customer service, and technical support on par with Robinhood and Revolut, all driven by decentralized blockchain technology. If our product experience can reach this level, HelloTrade can attract millions of first-time on-chain users.

The second advantage is our team. Stock capital markets and the crypto market are very different. The stock market has corporate actions (such as dividends, stock splits, mergers, etc.) and market closures, situations that are complex and nonexistent in the crypto field. To navigate these differences effectively, strong technical capabilities are needed. The three early engineers we have hired are all former founders of crypto DEXs.

Usually, a team either understands crypto or understands traditional finance, rarely both. However, our team has years of hands-on experience in both fields, and we believe this is also our unique advantage.

BlockBeats: You had a very successful career at BlackRock. For HelloTrade, what scale do you hope to achieve? What do you think is the key KPI for HelloTrade's success?

Kevin: That's a great question. I think our KPI will evolve over time.

Currently, we are more focused on Daily Active Users (DAU). Traditional KPIs such as trading volume and open interest are also essential, and we will set specific goals and monitor them closely as we progress.

But as I mentioned earlier, we want to be more than just a perpetual contract exchange. We aim to be the app that users habitually open every morning. They can not only trade on our app but also read news, receive price alerts, track important events like the FOMC meeting, inflation data, PCE, interest rate changes, and more here.

For me, the truly key metrics are daily active users, user engagement within the app, and which features users are utilizing. These metrics may not all directly translate to revenue, but they reflect user engagement. The more time users spend on the app, the more interaction there is, the stronger our relationship with the customer becomes. In the long run, this relationship is our most valuable asset.

Web3's Technological Foundation, Web2's Product Experience

BlockBeats: After discussing the product, let's talk about the technical implementation. Why did you choose MegaETH as the underlying infrastructure? Instead of selecting Solana, Base, Arbitrum, which had a more mature ecosystem at the time?

Kevin: There are three core reasons.

The first is performance. We wanted to build a trading system that can rival top traditional brokerages, with speed and user experience being top-notch. This requires a highly performant and reliable chain. Our team thoroughly researched many Layer 1 and Layer 2 solutions, conducted extensive testing, and MegaETH emerged as the highest performing choice. We plan to introduce some functionalities that were previously infeasible on the blockchain, all of which rely on MegaETH's throughput.

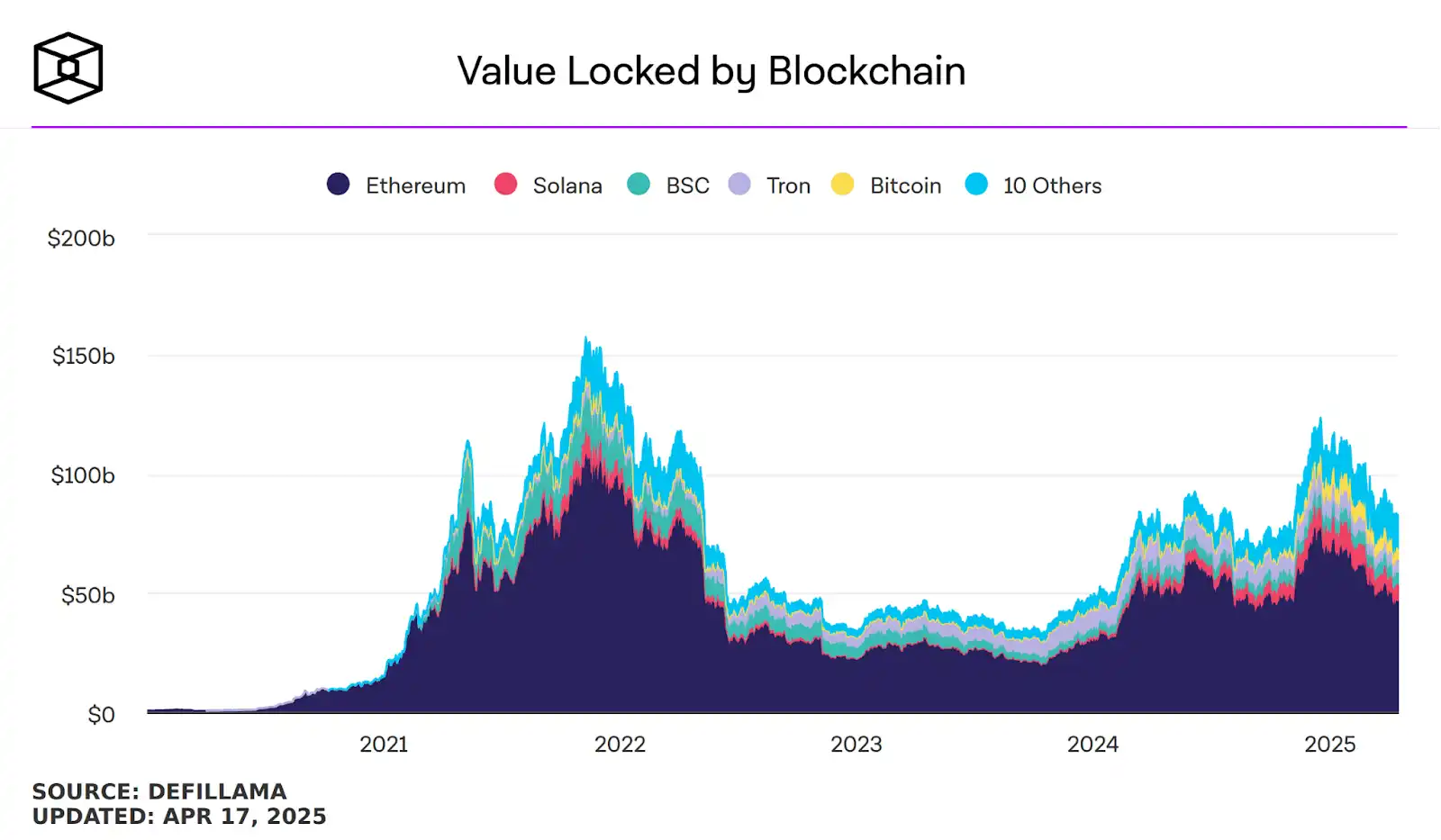

The second reason is my belief in Ethereum and its network effects. I have always believed that Ethereum's security, neutrality, and ecosystem richness are unparalleled to date. The future global financial and DeFi ecosystem will still be built around Ethereum as its core, with MegaETH serving as a "high-speed processing layer" within this core. For us, this combination makes a lot of sense. It inherits Ethereum's security while providing an extremely fast execution environment.

Ethereum TVL Compared to Other Chains|Image Source: DeFi Llama

Lastly, the MegaETH team is also a crucial factor. Many blockchain projects start with ambitious plans but struggle to materialize them. The MegaETH team are true builders, they have a long-term vision and the execution capability to bring plans to reality.

BlockBeats: To achieve an experience comparable to Web2, your mobile app is described as having no wallet setup, no gas fees, and no technical jargon. How was this achieved technically?

Kevin: For mass adoption of decentralized applications to achieve a Web2-like experience, several hurdles need to be overcome: wallet setup, gas fees, and fiat on/off-ramp. We will gradually address these issues.

Firstly, we will eliminate the need for gas fees, so users do not have to worry about transaction costs. Secondly, for users less familiar with Web3, we will collaborate with embedded wallet service providers to allow users to create wallets directly with their email. For more advanced users, we will also support connecting their own self-custody wallets.

The final challenge is how to onboard funds onto the platform. We are actively integrating fiat on/off-ramp channels to make the entire experience feel like using a traditional brokerage app—familiar and seamless.

BlockBeats: A good trading platform cannot do without liquidity. How do you plan to attract liquidity providers?

Kevin: The first key to attracting liquidity providers is to create a powerful product. If your product truly has many users trading on it, liquidity will naturally follow. Liquidity providers go where the trading action is, so our primary goal is to provide a product that generates real demand.

The second factor is the liquidity during traditional market closures such as weekends and after-hours, an area where blockchain can bring something new. This period experiences lower liquidity, and we are developing a unique incentive system to make providing liquidity during non-trading hours more cost-effective for liquidity providers, ensuring that our market remains deep, stable, and reliable 24/7.

Blockbeats: What do you think is the biggest challenge in building stock or ETF perpetual contract products? Is it compliance issues, the technical details you mentioned earlier, or user growth and education?

Kevin: The biggest challenge is addressing the issue of "24/7 trading," how to make a stock capital market, fundamentally different from crypto, adapt to the 24/7 uninterrupted operation of the crypto system.

Specifically, after-hours and weekend pricing is a technical challenge. We will combine external price feeds, Friday closing prices, and the weekend order book data itself. Additionally, we will collaborate with traditional financial participants over weekends to make the marking price more accurate and predictive.

Frankly, there is no perfect solution before the Nasdaq and NYSE truly achieve 24/7 trading. Yet, I find it very interesting that as these 24/7 stock perpetual contract platforms mature, they will become the main venues for weekend price discovery, and liquidity will deepen. By then, many traditional financial institutions will need to trade on these platforms over the weekend due to fiduciary duties.

The second challenge is user experience. Although we cannot reveal too much at this time, we will not only be doing perpetual contracts. Perpetual contracts may not be suitable for everyone. We plan to gradually introduce some lower-risk products that may still offer leverage, but the user's punishment when the price trend is unfavorable will be much smaller.

BlockBeats: Finally, let's talk about risk. At BlackRock, there is a saying: "It takes decades to build trust, but only a few minutes to lose it." At HelloTrade, what is your most concerning "few minutes scenario"?

Kevin: Our top priority is the safety of clients' assets and unexpected market conditions.

First is the security of client assets. We have all seen what has happened on FTX and some other platforms. Protecting users through proper asset segregation, robust risk controls, and secure DeFi infrastructure is our top priority. This is the cornerstone of trust and the most serious matter we take.

Secondly, we must be prepared for extreme scenarios. We are very confident in HelloTrade's core trading model under normal circumstances, but what truly makes us vigilant is a 1% probability "black swan" event like October 10. We are simulating and backtesting these extreme market conditions and embedding contingency plans and protective measures to ensure that our system remains stable and reliable even under extreme pressure.

In traditional finance, price range limits and circuit breaker mechanisms have existed for many years for a reason. They can prevent a complete market collapse in extreme situations, and we are also making efforts to prepare for these extreme scenarios.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.