- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

Earn

Earn- More

Digital banks have long ceased to make money from traditional banking services; the real goldmine lies in stablecoins and identity authentication.

Original Article Title: Neobanks Are No Longer About Banking

Original Article Author: Vaidik Mandloi, Token Dispatch

Original Article Translation: Chopper, Foresight News

Where Is the True Value Flowing for Digital Banks?

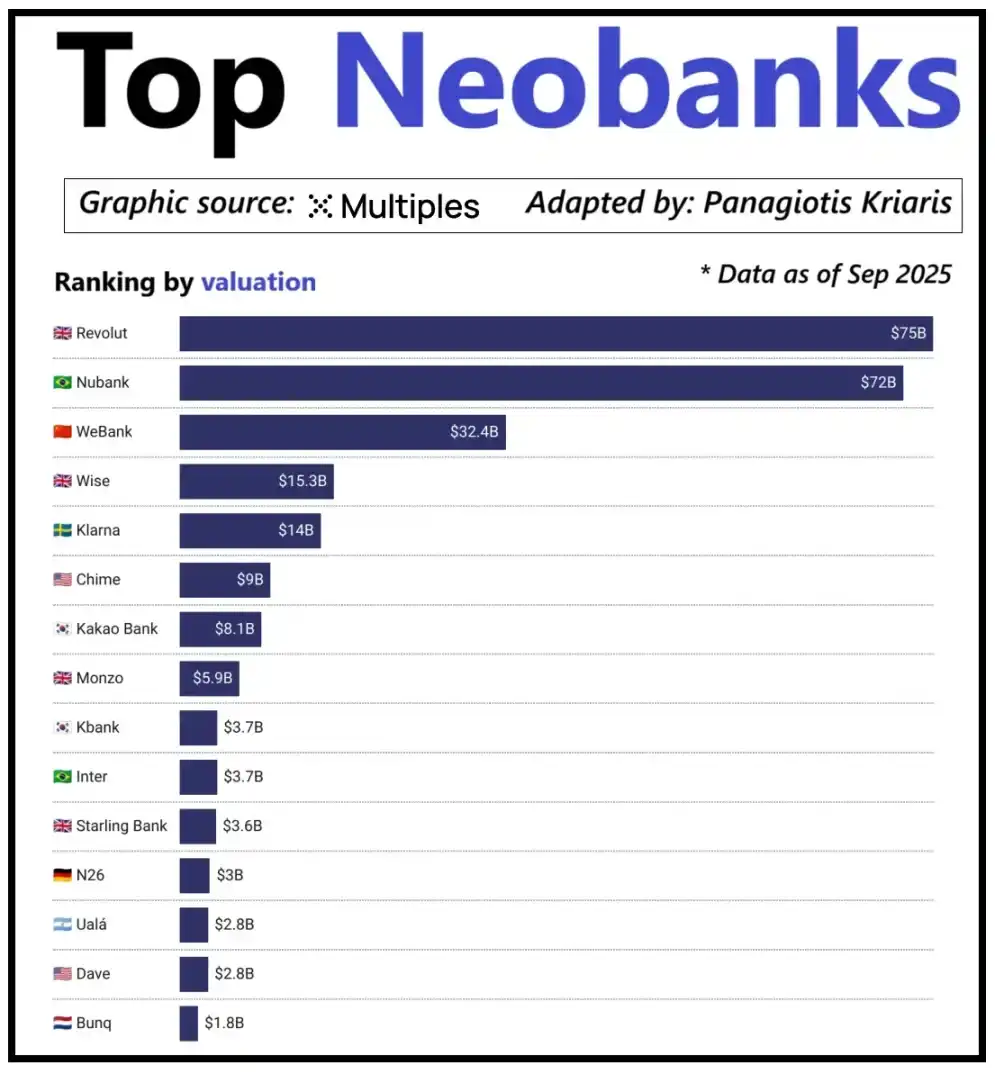

Looking at the top digital banks globally, their valuation is not simply determined by user scale but by their ability to generate revenue per user. Digital bank Revolut is a prime example: despite having fewer users than Brazilian digital bank Nubank, its valuation surpasses the latter. The reason lies in Revolut's diversified revenue streams, covering areas such as foreign exchange trading, securities trading, wealth management, and premium membership services. In contrast, Nubank's business expansion relies mainly on credit operations and interest income rather than bank card fees. China's WeBank has taken a different path of differentiation, achieving growth through extreme cost control and deep integration into the Tencent ecosystem.

Valuation of Top Emerging Digital Banks

Currently, crypto digital banks are experiencing a similar development milestone. The combination of "wallet + bank card" can no longer be called a business model, as any institution can easily launch such services. The platform's competitive advantage lies precisely in its chosen core monetization path: some platforms earn interest income from user account balances, some rely on stablecoin transaction volume for profits, and a few platforms place their growth potential in stablecoin issuance and management, as this is the most stable and predictable source of income in the market.

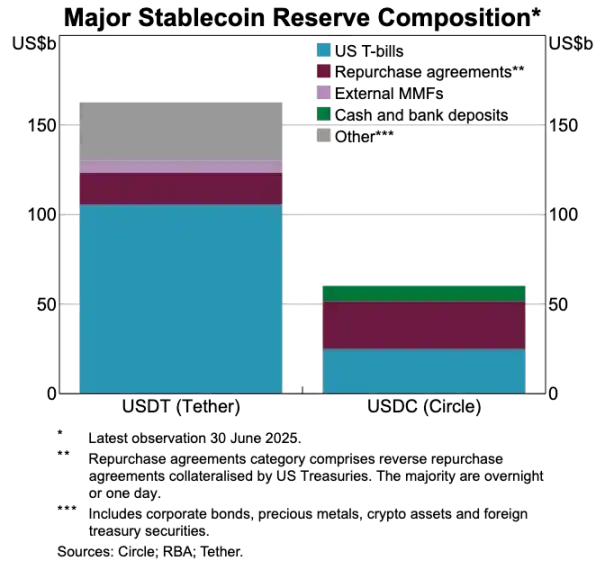

This also explains why the importance of the stablecoin race is becoming increasingly prominent. For reserve-backed stablecoins, their core profit comes from investment returns on reserves, i.e., the interest generated by investing reserves in short-term government bonds or cash equivalents. This income belongs to the stablecoin issuer rather than just the digital bank providing stablecoin holding and spending functions to users. This profit model is not unique to the crypto industry: in the traditional financial sector, digital banks also cannot earn interest from user deposits, and the actual custodian banks holding the funds enjoy this income. With the emergence of stablecoins, this "separation of income ownership" model has become more transparent and centralized, where entities holding short-term government bonds and cash equivalents earn interest income, while consumer-facing applications are primarily responsible for user acquisition and product experience optimization.

As the adoption of stablecoins continues to grow, a contradiction is gradually emerging: application platforms that undertake user acquisition, transaction matching, and trust building often cannot profit from the underlying reserve. This value gap is forcing enterprises to integrate into vertical domains, moving away from a mere frontend tool positioning towards the core of fund custody and management.

It is precisely due to this consideration that companies like Stripe and Circle have been increasing their efforts to lay out their strategies in the stablecoin ecosystem. They are no longer satisfied with staying at the distribution level but are expanding into the settlement and reserve management field, as this is the core profit-making area of the entire system. For example, Stripe launched its dedicated blockchain called Tempo, specifically designed for low-cost, instant transfers of stablecoins. Stripe did not rely on existing public blockchains like Ethereum or Solana but built its own transaction channels to control the settlement process, fee pricing, and transaction throughput, all of which directly translate into better economic benefits.

Circle has also adopted a similar strategy by creating a dedicated settlement network called Arc for USDC. Through Arc, inter-institution USDC transfers can be completed in real-time without causing congestion on the public chain network, nor incurring high fees. Essentially, Circle has built an independent USDC backend system through Arc, no longer being dependent on external infrastructure.

Privacy protection is another important driver of this strategy. As Prathik elaborated in the article "Reshaping the Brilliance of Blockchain," a public blockchain records every stablecoin transfer on a publicly transparent ledger. This feature is suitable for an open financial system but has drawbacks in commercial scenarios such as salary payments, supplier payments, and treasury management. In these scenarios, transaction amounts, counterparties, and payment patterns are sensitive information.

In practice, the high transparency of public chains allows third parties to easily reconstruct a company's internal financial situation through blockchain explorers and on-chain analysis tools. The Arc network enables inter-institution USDC transfers to settle outside of the public chain, preserving the advantage of fast stablecoin settlement while ensuring the confidentiality of transaction information.

Comparison of USDT and USDC Asset Reserves

Stablecoins Are Disrupting the Old Payment System

If stablecoins are at the core of value, the traditional payment system appears increasingly outdated. The current payment process involves multiple intermediaries: the receiving gateway is responsible for fund collection, the payment processor completes transaction routing, card networks authorize transactions, and the account-holding banks of the transaction parties ultimately settle. Each step incurs costs and causes transaction delays.

Stablecoins, on the other hand, bypass this lengthy chain of intermediaries. Stablecoin transactions do not require card networks or acquirers and do not need to wait for batch settlement windows. Instead, they are based on the underlying network to facilitate direct peer-to-peer transfers. This feature has a profound impact on digital banks, as it completely changes users' experience expectations. If users can achieve instant fund transfers on other platforms, they will not tolerate the cumbersome and costly transfer processes within digital banks. Digital banks either need to deeply integrate stablecoin transaction channels or risk becoming the least efficient part of the entire payment chain.

This transformation also reshapes the business model of digital banks. In the traditional system, digital banks could earn stable fee income through bank card transactions because the payment network firmly controlled the core of transaction flow. However, in the new system dominated by stablecoins, this profit margin has been greatly compressed. Since stablecoin peer-to-peer transfers do not have transaction fees, digital banks relying solely on bank card spending for revenue are facing a completely fee-less competitive track.

Therefore, the role of digital banks is shifting from card issuers to payment routing layers. As payment methods shift from bank cards to stablecoin direct transfers, digital banks must become the core circulation nodes of stablecoin transactions. Digital banks that can efficiently process stablecoin transaction flows will dominate the market because once users see them as the default channel for fund transfers, it is challenging to switch to other platforms.

Identity Authentication is Becoming the New Generation Account Carrier

As stablecoins make payments faster and cheaper, another equally important bottleneck is gradually emerging: identity authentication. In the traditional financial system, identity authentication is a separate process: banks collect user documents, store information, and conduct verifications in the background. However, in the scenario of instant wallet fund transfers, every transaction relies on a trusted identity authentication system. Without this system, compliance checks, anti-fraud controls, and even basic permission management are not possible.

For this reason, identity authentication and payment functionality are rapidly converging. The market is gradually moving away from separate KYC processes on each platform and shifting towards a portable identity authentication system that can be used across services, countries, and platforms.

This transformation is unfolding in Europe, where the EU digital identity wallet has entered the implementation phase. The EU no longer requires each bank or application to independently conduct identity verification; instead, it has created a government-endorsed unified identity wallet that all residents and businesses can use. This wallet is used not only for identity storage but also carries various authenticated credentials (such as age, residency proof, licensing qualifications, tax information, etc.), supports users in signing electronic documents, and has built-in payment functions. Users can complete identity verification, share information on demand, and payment operations in a single process, achieving full-process seamless integration.

If the EU Digital Identity Wallet is successfully implemented, the entire European banking architecture will be restructured: Identity authentication will replace bank accounts as the core entry point for financial services. This will make identity authentication a public good, and the distinction between traditional banks and digital banks will be weakened, unless they can develop value-added services based on this trusted identity system.

The crypto industry is also evolving in the same direction. Experiments related to on-chain identity authentication have been conducted for many years. Although there is currently no perfect solution, all explorations point to the same goal: to provide users with a means of identity verification that allows them to prove their identity or relevant facts without limiting the information to a single platform.

Here are several typical examples:

· Worldcoin: Building a global-scale identity proof system that verifies users' real human identity without revealing their privacy.

· Gitcoin Passport: Integrating various credentials and verifications to reduce the risk of sybil attacks in governance voting and reward distribution processes.

· Polygon ID, zkPass, and ZK-proof frameworks: Supporting users in proving specific facts without revealing underlying data.

· Ethereum Name Service (ENS) + off-chain credentials: Allowing crypto wallets to not only display asset balances but also associate users' social identities and authentication attributes.

The goal of most crypto identity authentication projects is consistent: to enable users to autonomously prove their identity or relevant facts, and ensure that identity information is not locked into a single platform. This aligns with the EU's vision of a digital identity wallet: an identity credential that can freely flow between different applications with no need for revalidation.

This trend will also transform the operating model of digital banks. Today, digital banks see identity authentication as a core control mechanism: user registration, platform audits, ultimately forming an account subordinate to the platform. However, when identity authentication becomes a credential that users can autonomously carry, the role of digital banks shifts to being a service provider accessing this trusted identity system. This will simplify the user onboarding process, reduce compliance costs, minimize redundant verification, and allow crypto wallets to replace bank accounts as the core vessel for user assets and identity.

Future Development Trends Outlook

In conclusion, the former core elements of the digital banking system are gradually losing their competitive edge: user scale is no longer a moat, bank cards are no longer a moat, and even a streamlined user interface is no longer a moat. The real differentiation competitive barriers are reflected in three dimensions: the profit products chosen by digital banks, the fund flow channels they rely on, and the identity authentication system they access. Apart from these, other functions will gradually converge, and substitutability will become stronger.

The future successful digital banks will not be lightweight versions of traditional banks, but rather wallet-first financial systems. They will anchor on a core profit engine, which directly determines the platform's profit margin and competitive moat. Overall, the core profit engine can be divided into three categories:

Interest-Driven Digital Bank

The core competitiveness of these platforms is to become the preferred channel for users to hold stablecoins. As long as they can attract a large number of user balances, the platform can earn income through reserve-backed stablecoin interest, on-chain rewards, staking, and re-staking, without relying on a large user base. The advantage lies in the fact that the profit efficiency of asset holding is much higher than that of asset circulation. These digital banks may seem like consumer-facing applications, but they are actually modern savings platforms disguised as wallets, with the core competitiveness of providing users with a seamless interest-earning experience.

Payment Flow-Driven Digital Bank

The value proposition of these platforms comes from transaction volume. They will become the primary channel for users to send and receive stablecoin payments, and for consumption, deeply integrating payment processing, merchants, fiat-to-crypto exchanges, and cross-border payment channels. Their profit model is similar to that of global payment giants—thin profit margins per transaction, but once they become the user's preferred fund transfer channel, they can accumulate substantial income through a large transaction volume. Their moat is user habits and service reliability, becoming the default choice when users need to transfer funds.

Stablecoin Infrastructure-Driven Digital Bank

This is the deepest and potentially highest-reward track. These digital banks are not just channels for stablecoin circulation but are dedicated to controlling the issuance of stablecoins, or at least controlling their underlying infrastructure, with business scopes covering stablecoin issuance, redemption, reserve management, and settlement, among other core processes. The profit potential in this field is the most lucrative because control over the reserve directly determines income attribution. These digital banks integrate consumer-side functions with infrastructure ambitions, evolving towards a full-fledged financial network rather than just applications.

In short, Interest-Driven Digital Banks make money from user deposits, Payment Flow-Driven Digital Banks make money from user transactions, and Infrastructure-Driven Digital Banks can generate continuous profits regardless of user actions.

I anticipate that the market will diverge into two major camps: the first camp consists of consumer-facing application platforms that mainly integrate existing infrastructure, offer simple and user-friendly products, but have extremely low user conversion costs. The second camp moves towards the core area of value aggregation, focusing on stablecoin issuance, transaction routing, settlement, and identity verification integration, among other businesses.

The latter's positioning will no longer be limited to applications but as infrastructure service providers disguised in consumer-facing attire. Their user stickiness is extremely high as they quietly become the core systems for on-chain fund circulation.

You may also like

Solana Loses Major Portion of Validators as Smaller Nodes Exit: Concerns Over Centralization

Key Takeaways: Solana has experienced a significant drop in active validators from a high of 2,560 in March…

Gold Price Prediction as Tom Lee Says Metals Rally Could Hit Crypto

Key Takeaways: Gold recently reached an all-time high of $5,598, reflecting a strong investor shift towards safe-haven assets…

Bitcoin Price Prediction: Binance Inflows Just Hit a 4-Year Low – Violent Move Above $100K is Next

Key Takeaways: Bitcoin inflows into Binance have dropped to their lowest in four years, potentially signaling a tight…

Russia Caps Crypto Investments at $4,000 Annually for Non-Qualified Investors – Will Others Follow Suit?

Key Takeaways Russia’s proposal sets a $4,000 annual investment limit for non-qualified crypto investors, sparking discussions on regulatory…

Crypto Price Prediction for January 28 – XRP, Solana, Bitcoin

Key Takeaways Bitcoin price recently hit $90,000 but struggled to maintain this peak. XRP and Solana are following…

We Hacked China’s Alibaba AI to Predict the Price of XRP, Solana and Dogecoin By the End of 2026

Key Takeaways Alibaba’s AI model, KIMI, forecasts significant price increases for XRP, Solana, and Dogecoin by the end…

US Senators Criticize DOJ Over Crypto Crime Unit Closure Amid Financial Conflict Concerns

Key Takeaways: Six US senators have criticized Deputy Attorney General Todd Blanche for shutting down the DOJ’s crypto…

Why Is Crypto Down Today? – January 29, 2026

Key Takeaways The crypto market has fallen by 1.7% over the past 24 hours, with significant declines in…

Solana Price Prediction: Leading Crypto Firm Reduces SOL ETF Exposure – Should Investors Be Concerned?

Key Takeaways Digital Currency Group (DCG) has recently sold significant Solana holdings, sparking discussions on potential future price…

Ethereum Price Prediction: Wall Street Firm Begins to Buy and Lock ETH – Is This Brave or Insane?

Key Takeaways BitMine’s significant investment in Ethereum by securing 4.2 million ETH and staking 2.2 million ETH showcases…

XRP Price Prediction: Price Looks Stagnant – But This Key Signal Just Flashed Green After Months

Key Takeaways Recent indicators suggest a potential bullish trend for XRP, indicating a possible price surge. Traders have…

![[LIVE] Crypto News Today: Latest Updates for Jan. 23, 2026 – BTC Slides Below $90K as Crypto Market Extends Broad Sell-Off](https://weex-prod-cms.s3.ap-northeast-1.amazonaws.com/medium_21_2c30f7df62.png)

[LIVE] Crypto News Today: Latest Updates for Jan. 23, 2026 – BTC Slides Below $90K as Crypto Market Extends Broad Sell-Off

Key Takeaways The crypto market is in a downward trend, with GameFi, AI, and RWA sectors showing some…

Solana Price Prediction: 200+ U.S. Stocks Just Landed on SOL – Is This the Most Bullish News of the Year?

Key Takeaways: Solana has integrated over 200 tokenized U.S. stocks and ETFs, enhancing its status as the preferred…

XRP Price Prediction: $1.88 Triple-Bottom Support Amid ETF Money Pull Back – Analyzing Future Directions

Key Takeaways XRP currently stabilizes around $1.88 with triple-bottom support after recent price slips below $2.00. Institutional ETF…

Crypto Price Prediction Today 22 January – XRP, Solana, Sui

Key Takeaways XRP Price Outlook: XRP remains in a fragile state within a descending channel, with the $1.80…

Cryptocurrency Price Prediction Today 23 January – XRP, Bitcoin, Ethereum

Key Takeaways Bitcoin, Ethereum, and XRP are in distinct phases of consolidation or resistance, with potential for significant…

Ethereum Launches $2M Quantum Defense Team as Threat Timeline Accelerates

Key Takeaways Ethereum has prioritized quantum resistance by establishing a dedicated Post Quantum (PQ) team, allocating $2 million…

Bitcoin & Ethereum ETFs Shed Over $1Billion, Solana and XRP Attract Inflows

Key Takeaways Bitcoin and Ethereum ETFs experienced substantial outflows exceeding $1 billion in just one day, reflecting a…

Solana Loses Major Portion of Validators as Smaller Nodes Exit: Concerns Over Centralization

Key Takeaways: Solana has experienced a significant drop in active validators from a high of 2,560 in March…

Gold Price Prediction as Tom Lee Says Metals Rally Could Hit Crypto

Key Takeaways: Gold recently reached an all-time high of $5,598, reflecting a strong investor shift towards safe-haven assets…

Bitcoin Price Prediction: Binance Inflows Just Hit a 4-Year Low – Violent Move Above $100K is Next

Key Takeaways: Bitcoin inflows into Binance have dropped to their lowest in four years, potentially signaling a tight…

Russia Caps Crypto Investments at $4,000 Annually for Non-Qualified Investors – Will Others Follow Suit?

Key Takeaways Russia’s proposal sets a $4,000 annual investment limit for non-qualified crypto investors, sparking discussions on regulatory…

Crypto Price Prediction for January 28 – XRP, Solana, Bitcoin

Key Takeaways Bitcoin price recently hit $90,000 but struggled to maintain this peak. XRP and Solana are following…

We Hacked China’s Alibaba AI to Predict the Price of XRP, Solana and Dogecoin By the End of 2026

Key Takeaways Alibaba’s AI model, KIMI, forecasts significant price increases for XRP, Solana, and Dogecoin by the end…